Automated Underwriting: How to Improve Process and Customer Experience

What is automated underwriting and how does it help insurers speed up processes and enhance customer experience? Here’s expert advice on how to reap the benefits of automated insurance underwriting.

What is automated underwriting?

Insurers use automated underwriting technology to make faster and more precise underwriting decisions, resulting in improved efficiency and profitability. But more than that, automated underwriting represents a trend that will play a critical role in the insurance industry's future growth and success.

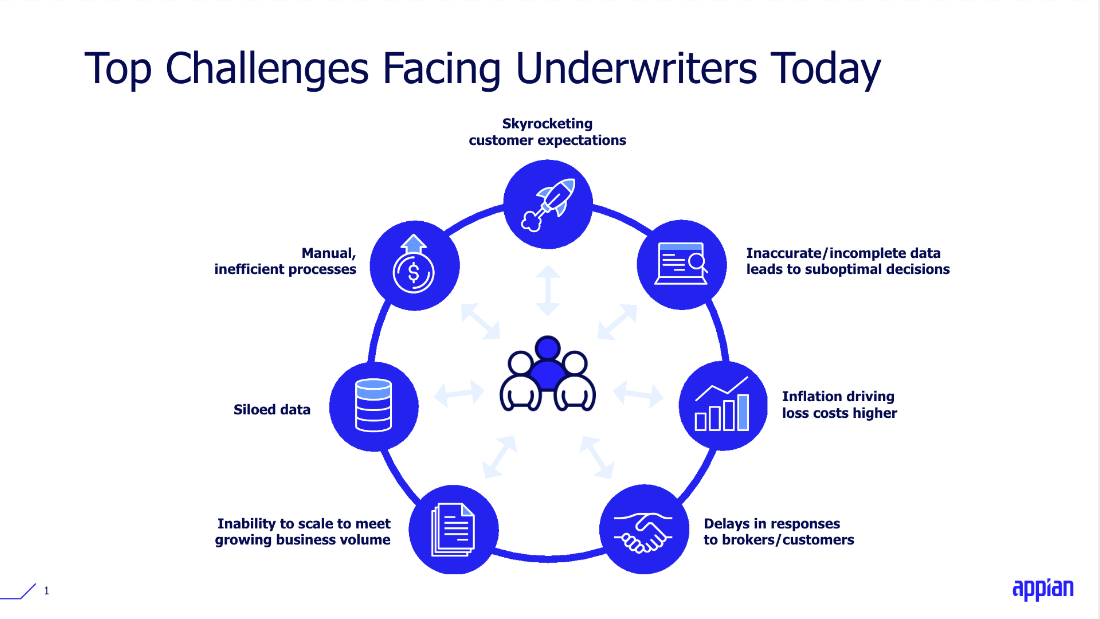

Here’s why: customers are increasingly demanding the speed and convenience of a first-rate digital experience. Currently, only 15% of customers say they are satisfied with the digital experience their insurer provides, and customers under the age of 55 are nearly three times more likely to switch insurers for better digital tools than those who are 55+. So the big question for today’s insurers is: How can you improve your workflows to meet high customer expectations and return quotes faster than the competition?

The big question: How can you improve your workflows to meet high customer expectations and return quotes faster than the competition?

But manual processes often stand in the way of making those improvements. Underwriters may spend as much as 40% of their time on manual tasks (such as gathering and entering data for submissions, renewals, and the like), representing a staggering $85 to $160 billion in efficiency loss over the next five years. But with automated underwriting tools, it doesn’t have to be that way.

Now is also a great time to reexamine what automated insurance underwriting tools can do to improve process speed. Recession anxiety coupled with rising interest rates—not to mention the growing severity of natural disasters and weather-related losses—are stress testing the underwriting processes of insurers everywhere. Insurers are also dealing with understaffed IT teams that lack the bandwidth to keep up with growing customer expectations and rising demand for legacy system modernization. To overcome these challenges, insurers are betting on more advanced systems—using technologies like artificial intelligence and machine learning—to accelerate underwriting processes and outmaneuver competitors.

Process and system modernization are also top of mind for insurers, according to a recent survey by analyst firm Gartner. Insurers are sharpening their focus on back-office modernization to optimize the customer experience and overcome limitations on straight-through processing (STP). More than half of insurance industry CIOs plan to increase their technology investments in 2023, with the most common area of focus being application modernization, Gartner reported. All of this means automated underwriting is a trend that isn’t going anywhere.

Why automated insurance underwriting matters

Manually coordinating data acquisition, managing multiple versions of spreadsheets, and entering and re-entering data across many different systems can overwhelm already stretched underwriting resources. Also, efforts to win new business may be stalled by added time and complexity in the analysis and pricing process.

Does that mean automation will overtake the core responsibilities of the human underwriter? No, but automation will augment the capabilities of underwriters by eliminating mundane, repetitive tasks and freeing them up to focus on more high-impact work.

To improve customer experience while controlling risk, leading insurers are rethinking traditional approaches to underwriting by modernizing legacy systems and equipping underwriters with better visibility into the data they need to make faster, more informed risk-related decisions. You’ll need to adapt to keep up. Here are some of the benefits insurers are seeing from incorporating automation into underwriting:

Top ways automated underwriting systems streamline processes

Reduced technical debt

In an increasingly digital world, innovation is a critical success factor. In fact, innovation ranks among the top two priorities for C-suite executives across industries, according to McKinsey. But legacy systems can get in the way of innovation. Insurers that do a better job of automating processes and adding value to the underwriting value chain will come out on top. That is why eliminating technical debt should be an essential part of any system modernization strategy, so says a recent survey by Deloitte.

For context, it’s worth noting the case of one insurance company where technical debt amounted to as much as 60% of every dollar spent on IT. If digital underwriting continues to go mainstream, it could drive higher levels of revenue, underwriting profitability, and next-level customer experience, according to analyst firm Gartner.

So, how have industry decision makers responded to this challenge? Many took it as a wake-up call, according to data from a recent CIO survey by Celent:

- 73% of large carriers now use the cloud as part of their underwriting solutions

- 64% of large carriers now use insurtech for underwriting

- 85% of medium-sized carriers use underwriting vendors

Bottom line: Legacy system modernization is key to minimizing technical debt and transforming the underwriting value chain so insurers can quickly adapt to fast-changing risk patterns and customer expectations now and in the future.

Connected workflows, faster decisions

Perhaps the triple crown of automated underwriting technology is its ability to connect workflows, unify disparate data sources, and reduce decision-making time. This powerful trio of benefits enables customers to apply for a policy and receive a quote faster. Not to mention that automated underwriting solutions can be easily integrated with existing legacy systems (e.g., policy administration) and even advanced third-party data sources, such as IoT devices and telematics. All of this allows for a more informed and seamless end-to-end underwriting experience.

Improved customer insights

Automated underwriting augments insurers’ ability to rapidly collect, ingest, and analyze large amounts of customer information, including demographic data, loss runs, ACORD forms, and more. This is essential for accelerating speed to quote and standing out in a competitive market.

Data integration challenges have traditionally held insurers back from rooting out inefficiencies as they struggled to unlock a single view of customer information and quote, rate, and bind new business faster. This is where a process automation platform with data fabric capabilities comes into play as a better way to streamline underwriting workflows, tame technical debt, and unify data silos.

A data fabric can give underwriters a real-time view of all the information they need in one place, streamlining workflows, including underwriting desktops, rules and modeling solutions, policy administration systems, CRMs, and billing and claims systems.

5 key benefits of an automated underwriting process

Insurers must strike a careful balance between speed and accuracy when it comes to the underwriting process. That’s the advantage of having an underwriting workbench powered by a process automation platform and a data fabric.

It’s the fastest, easiest way to combine data from multiple, disconnected systems and create a single source of truth for underwriters while automating data ingestion and clearance and triage of submissions.

In thinking about the challenges of scaling complex insurance workflows to meet emerging threats and ever-rising customer expectations, it’s worth exploring the top five benefits of an automated underwriting process:

1. Increased efficiency

One of the key advantages of automated underwriting is increased speed and cost efficiency. By automating the collection and analysis of data, insurers can reduce the time and effort required to underwrite a policy. Perhaps the biggest takeaway is that process automation not only saves time and money but also elevates the customer experience, as customers receive faster, more convenient service.

2. Improved accuracy

Automated systems can analyze massive amounts of data in real-time, using advanced algorithms and data analysis to speed informed underwriting decisions and reduce the risk of potential losses. For example, in a recent Celent study, 69% of paper applications received by study participants were NIGO (not in good order, in other words, submitted with missing or inaccurate information). NIGO paperwork drives up costs as insurers, brokers, or intermediaries have to go back and try to contact the customer, resulting in delays. In contrast, insurers offering electronic applications and a digital experience benefitted from an NIGO rate that fell to just 5%.

3. Better customer experience

The faster you can quote, rate, and bind, the more likely you are to win new business. The longer it takes, the more likely it is that the customer will sign with another provider with a more customer-centric process and digital experience, increasing your not taken up (NTU) ratio.

Likewise, automated underwriting also offers a more convenient way to serve customers. For the benefits of speed and convenience, 48% of customers prefer opening a new account or product on their computer and 34% prefer using a mobile app. In other words, speed and convenience are golden in the underwriting business.

4. Reduced costs

Automating underwriting processes could allow insurers to reap the benefits of $160 billion in efficiency gains by 2027, according to Accenture. By streamlining the underwriting process and reducing the likelihood of errors, insurers can reduce the time and resources required to underwrite a policy, which reduces costs. Additionally, by using advanced analytics to price policies more accurately, insurers can increase their profitability and reduce the likelihood of losses.

5. Standing out from the crowd

Integrated technology coupled with automated, streamlined underwriting allows digital leaders to differentiate themselves in a crowded market by delivering a faster, more efficient, and more convenient underwriting process, ultimately enabling insurers to improve their quote-to-bind ratios.

7 ways automated underwriting enhances customer experience

Insurance customers have higher expectations than they did in the past. Policyholders expect the same digital convenience they experience in other aspects of their lives. The stakes have never been higher. Acquiring new customers costs nine times more than retaining existing ones. In other words, providing exceptional service and keeping current policyholders happy is more than a talking point, it’s a necessity.

And automation is redefining what it means to be customer-focused. It goes beyond coordinating data acquisition, managing umpteen versions of spreadsheets, and entering and re-entering data across numerous, disconnected systems, all of which consume underwriting time and add complexity to the customer journey. By automating the underwriting process, insurance companies can significantly reduce the time it takes to issue a policy and deliver a seamless customer experience.

Let’s recap seven top ways in which automated underwriting enhances the customer experience:

1. Speed

For starters, it can empower underwriters to do real-time data collection and analysis from multiple data sources, facilitating faster, more-informed decisions about the risk levels of potential policyholders.

In a world where the slow pace of legacy underwriting can be a turn-off for customers, automation can help traditional insurers compete with more nimble, digital-native challengers. And the stakes have never been higher. For example, the average close ratio across the P&C insurance industry is 55%, which means 45% of prospects were missed during the process. Which is another way of saying that 45% of prospects left without buying a product, resulting in lost opportunities and lost revenue for the insurer.

2. Accuracy

Automated underwriting systems use algorithms and artificial intelligence and machine learning to analyze large amounts of data, making the underwriting process more consistent and less error-prone. Customers can be sure that their policies are based on the most up-to-date and accurate information, helping to avoid any issues or disputes down the line.

3. Convenience

Automated underwriting systems allow customers to submit their applications electronically and receive quotes from the comfort of their own homes, 24/7. This eliminates the need for customers to meet with insurance agents in person, over the phone, or to take time off work to complete the application process.

4. Personalization

By making better use of their large data sets, insurers can make more informed and educated coverage recommendations. For instance, they could recommend bundling a new service, or if they know someone just got married or had a baby, they could send a note reminding them to revisit their policies to avoid any coverage gaps.

5. Transparency

Automated underwriting systems provide customers with a clear and transparent overview of the underwriting process, so they can understand the status of their application, how their policies are being calculated, and why they are receiving specific rates. This helps to build trust and confidence in the insurance industry, as customers can see for themselves how their policies are calculated. Automated underwriting also reduces the need for a customer to pick up the phone and inquire about their policy. That’s a win-win situation that saves customers the hassle of calling and decreases the number of calls insurers must handle.

6. Better customer service

Automated underwriting systems can free up insurance agents to spend more time serving customers rather than bogged down in manual, administrative tasks. This means that customers can receive more personalized and responsive customer service, helping to build lasting relationships with insurance companies.

7. Cost savings

Automated underwriting systems can help insurance companies increase underwriting productivity and efficiency and reduce their operating costs, which can translate into lower premiums and more competitive rates for customers.

With some digital-native insurtechs issuing policies and processing claims in seconds and minutes rather than days and weeks, customer expectations for traditional insurers will only grow. But as the list above shows, speed is just the start of the customer enhancements that automated underwriting can deliver.