Today underwriters spend 40% of their time on non-core activities, representing an efficiency loss of $85-$160 billion over the next five years.

We recently had the chance to sit down with Juan Mazzini, Head of Insurance Practice for APAC, EMEA, and LATAM at Celent, during InsureTech Connect Vegas to discuss how insurers can automate the underwriting process to increase speed to quote and improve the customer experience. Here’s a look at that conversation.

Automating the underwriting process to increase speed and improve customer experience.

What is driving the demand for a better, faster underwriting process?

Jake Sloan: Now is the time to break the rules and put forth bold strategies and technology that really complement the front-end and back-end legacy stack. You think about the different expectations today including the pandemic and the move to digital. Teams had to rapidly mobilize as they went into shelter in place/stay at home. There’s also growing expectations from the consumer. Today’s customers can see the status of their food as it’s being delivered and wonder why they can’t see the status of their underwriting application in real time online as well? Why can’t they have a more cohesive, digital experience?

When you think about the back side of things as well and all the manual, inefficient processes with underwriting today, there’s enormous opportunity for workflow optimization. There’s also significant pressure with profitability and you think about the storm patterns and worsening natural disasters from a combined ratio perspective. Another driver is insurers continue to find it difficult to recruit and retain talent for complex roles like underwriting. Even before the Great Resignation, the insurance industry faced a talent gap as it struggled to find replacements for its rapidly retiring workforce.

What does the underwriting and technology landscape look like today?

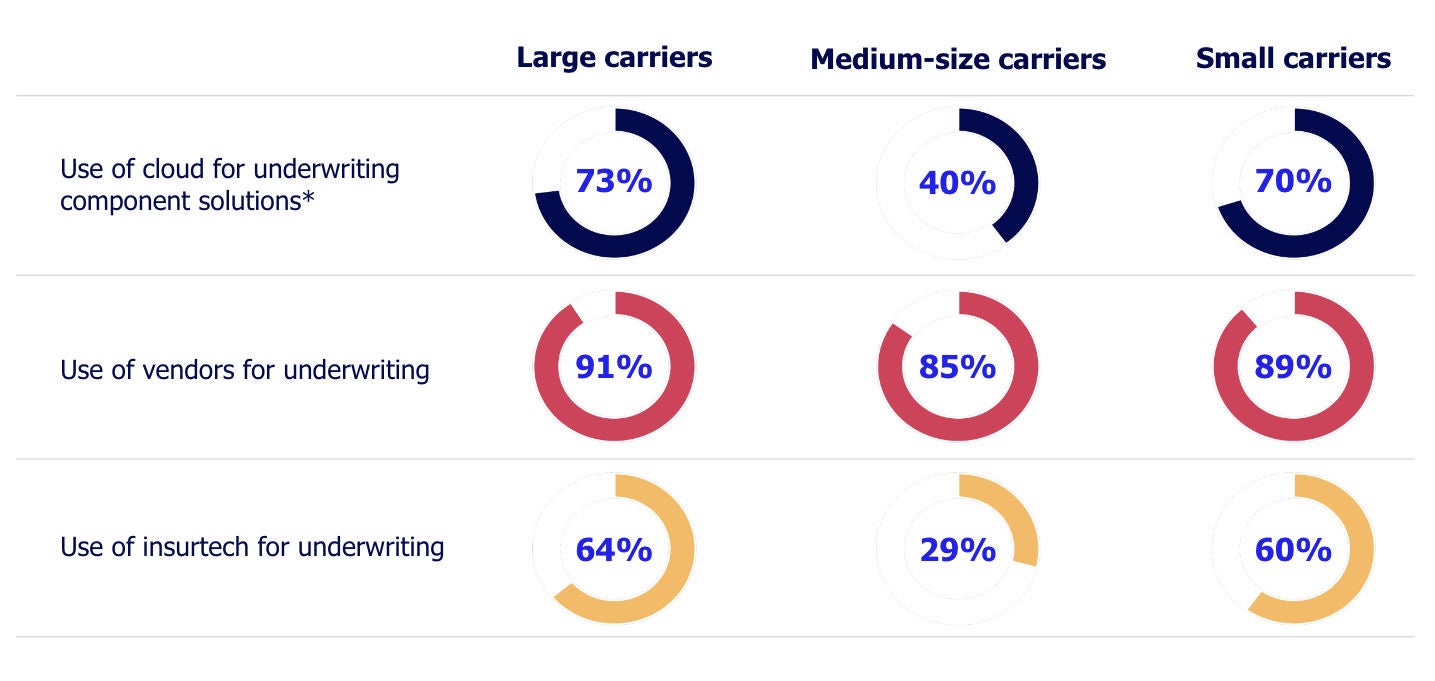

Juan Mazzini: Every year, Celent runs surveys around the world related to the use of technology in insurance. Data obtained from our North American survey shows there's a different pattern of behavior in terms of adoption of the cloud and use of insurtech startups to help improve the underwriting function depending on size of the carrier. Medium-sized carriers, for instance, are more likely to work with established vendors than insurtechs. And 40% of medium-size carriers are using the cloud for underwriting components. This is good news. Think about where we were five years ago in terms of the cloud.

Interestingly, small and large carriers share similar patterns in terms of cloud adoption, use of vendors for underwriting, and use of insurtech startups for underwriting. It looks like they are trying to experiment or combine different solutions that are complementary to improve the underwriting function.

Another thing that the hard data doesn’t show but comes up frequently in our conversations about underwriting is that carriers have more options. There are more vendors and solutions. There’s more competition and startups. As a result, we are going to see more and more advancement since there are more options.

Also, as a result of the pandemic, we had to digitize processes that could have been historically done physically. Many carriers found themselves in a situation where these applications were built 10–15 years ago and were difficult to digitize. We see more carriers looking into low-code/no-code platforms to not overhaul the entire core system, but to be able to provide a quick response to the needs of digitization and put some applications in front of those core systems to accelerate digital modernization.

Another thing we see is the use of more data and analytics for better underwriting. It doesn’t matter what part of the insurance value chain you are looking at, there’s something you can be doing better with data. Underwriting is a big area for improvement. And you can’t view the value chain in silos.

For example, there’s initiatives for using data in underwriting that have a positive effect in improving the customer experience and being able to provide opportunities for cross-sell and up-sell. A challenge, though, is how you manage and fulfill all this data while staying compliant with regulations. These regulations of course vary from geographies. We see Europe getting stricter with the use of data.

There are also more conversations about open insurance. Have you heard of open banking? In the United States, you didn’t need a regulation about open banking—you just did it. In Europe, they do have regulations for open banking and now they are considering the same for open insurance. Brazil was the first country in the world to regulate open insurance.

Based on the history of what has happened in the United States with open banking, I wouldn’t expect regulation for open insurance. But with what’s happening in Europe, and we’ve seen in Brazil so far, it levels the playing field since everyone needs to comply. Some of the investments in technology that carriers have been postponing, will have to be undertaken now since a regulator is asking for it. In the United States, it’s more about the competitive advantage of open insurance as a business model, which we see in the myriad of partnerships such as embedded insurance, marketplaces, platforms, and ecosystems. Managing the data will be increasingly important and crucial.

After all, data is the foundation and core of our business. We base all our decisions on data. Managing the data not only from the technology perspective, but from a culture standpoint and becoming a data-driven organization, that’s part of the issue. Another consideration when looking to optimize actuary and underwriting roles is that there are different use cases for life, health, and P&C. There are steps you can take now, starting with looking for data service providers out there and what you can do with IoT sensors. Sensors have enormous power to help us better understand risk in real time.

The other aspect is having platforms that will allow you to easily do API integrations. You need to be able to ingest the data very easily.

Want to hear the rest of the conversation?

Check out the full video with Jake Sloan and Juan Mazzini from InsureTech Connect Vegas.

About Celent

Celent is a research and advisory firm dedicated to helping financial institutions formulate comprehensive business and technology strategies. Celent publishes reports identifying trends and best practices in financial services technology and conducts consulting engagements for financial institutions looking to use technology to enhance existing business processes or launch new business strategies. With a team of internationally experienced analysts, Celent is uniquely positioned to offer strategic advice and market insights on a global basis. Celent is a member of the Oliver Wyman Group, which is a wholly-owned subsidiary of Marsh McLennan. [NYSE: MMC]. For more information, visit www.celent.com.